Quality Investing Simplified: ROE vs ROCE and Why it Matters?

Imagine you are buying a house to rent it out. You put down ₹20 lakhs of your own money and borrow ₹80 lakhs from the bank. If the house generates a rental income, you might calculate your return based only on the ₹20 lakhs you paid (your equity). The return looks huge, but does that number tell you how good the property actually is, or just how much debt you used to purchase the house?

This is exactly the dilemma investors face when choosing between Return on Equity (ROE) and Return on Capital Employed (ROCE). Both measure profitability, but one can sometimes mask high risk with high returns. In Quality Investing, understanding the distinction between these two metrics is the difference between buying a genuinely efficient business and falling into a debt-fueled trap.

What is ROE (Return on Equity)?

Return on Equity (ROE) is the investor’s favourite metric. It answers a simple question: For every rupee shareholders invested, how much profit did the company generate?

It focuses strictly on the owners' money.

Formula: Net Income / Shareholders’ Equity

From the perspective of Quality, a high and consistent ROE is a classic sign of a company that efficiently compounds wealth for its owners. It tells you how well the management is using your money.

What is ROCE (Return on Capital Employed)?

Return on Capital Employed (ROCE) takes a broader view. It answers: How much profit does the business generate using all the capital available to it (both money from shareholders and money borrowed from lenders)?

It assesses the efficiency of the entire business engine, regardless of where the fuel (money) came from.

Formula: Earnings Before Interest and Tax (EBIT) / Total Capital Employed (Equity + Debt)

ROCE is often considered a stricter measure of Quality because it penalises companies for holding inefficient cash or taking on too much unproductive debt.

The Critical Difference: The Debt Distortion

The main difference lies in how these measures treat debt. ROE can be misleading. If a company takes on massive loans to buy back shares or fund day-to-day operations, its shareholder equity base shrinks (or doesn't grow as fast), while profits might remain steady or grow slightly. This pushes the ROE up artificially. A company might look like a high-quality superstar with 25% ROE, but it might be sitting on a mountain of debt that makes it risky.

ROCE, however, includes that debt in the denominator. If a company loads up on debt, the Capital Employed increases. Unless the profit (EBIT) jumps significantly to justify that debt, the ROCE will drop.

- ROE says: Look how much money we made for you!

- ROCE asks: But how much debt did you take to do it?

Why This Distinction Matters to Investors

For investors and analysts focused on the Quality Factor, blindly chasing high ROE can lead to Quality Traps i.e. companies that look profitable but are actually financially fragile due to leverage.

- Avoiding the Leverage Trap: By comparing ROE and ROCE, investors can spot red flags. If ROE is rising (say 30%) but ROCE is mediocre (say 12%), it’s a clear signal that the returns are driven by debt, not operational strength.

- True Sustainability: High ROCE companies typically have a competitive advantage (or moat). They don't need excessive debt to grow. These are the survivors that tend to be resilient during market down-cycles better than those high-debt firms.

- Better Risk-Adjusted Returns: Focusing on ROCE helps select companies that are efficient allocators of capital. Historically, efficient capital allocation is a hallmark of multi-fold returns.

When to Use Which?

Understanding the suitability of each ratio is key to effective investment analysis and the selection of a true quality company.

- ROE is suitable for Financials and Asset-Light Sectors: For Banks and NBFCs, debt is a raw material, not just a liability. Hence, ROCE is less relevant. Similarly, for IT or FMCG companies with low to negligible debt, ROE and ROCE will often be very close, making ROE a sufficient measure.

- ROCE is suitable for Capital-Intensive Sectors: For industries like infrastructure, power, telecom, or manufacturing, where heavy capital expenditure and debt are common, ROCE is the ultimate truth-teller. It ensures that the heavy investment in assets is actually generating returns, not just fueled by loans.

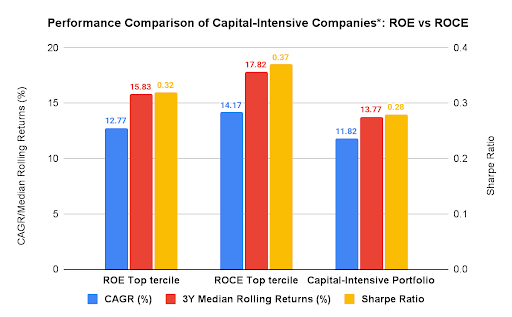

Source: NJ AMC's Internal Research, CMIE, NSE, NJ AMC's Proprietary SmartBeta Research Platform. Data is for the period 30th September, 2006 to 31st January, 2026. ROE Top Tercile and ROCE Top Tercile represent the top 33% stocks based on ROE and ROCE from the capital-intensive universe, respectively. Capital-Intensive Portfolio represents all the companies present in the capital-intensive universe. *Capital-intensive companies are defined as per NJ AMC’s Proprietary methodology. Past performance may or may not be sustained and is not indicative of future returns.

The chart clearly shows that in Capital-Intensive companies, the ROCE top-tercile portfolio delivers higher returns and better risk-adjusted performance than ROE in terms of CAGR (14.17% vs 12.77%) and Sharpe Ratio (0.37 vs 0.32).

It also shows stronger performance with higher 3Y median rolling returns (17.82% vs 15.83%), reinforcing why ROCE is the more reliable measure when heavy capital expenditure and debt are part of the business model.

Furthermore, ROE Top Tercile still outperforms the broader Capital-Intensive Portfolio (CAGR 12.77% vs 11.82%), with higher rolling returns and Sharpe too, implying that ROE isn’t a bad lens to start with.

However, for capital-intensive businesses, ROCE leads on both returns and risk-adjusted performance, which makes it a better metric to use over ROE in this case.

Summary Snapshot: Decoding the Key Differences

| Particulars | ROE (Return on Equity) | ROCE (Return on Capital Employed) |

| Simple Meaning | Measures how much profit the company generates using only the shareholders' money. | Measures how efficiently the company uses total capital (both shareholders' money + borrowed money). |

| The Core Question | For every rupee owners invested, how much did they earn? | For every rupee invested in the business (owned or borrowed), how much operating profit did it generate? |

| Formula | Net Income / Shareholders’ Equity | EBIT / Total Capital Employed (Equity + Debt) |

| Impact of Debt | Ignores debt in the denominator. High debt can artificially inflate ROE, making a risky company look highly profitable. | Includes debt in the denominator. It penalises companies for taking on unproductive debt. If debt rises without a profit jump, ROCE falls. |

| Suitable Sectors | Financials & Asset-Light: Best for non-lending financial companies (NBFCs, etc.), IT, and FMCG sectors. | Capital-Intensive: Best for Manufacturing, Infrastructure, Power, Telecom, and Auto sectors, where heavy machinery and debt are used. |

| What It Signals | Profitability for Owners: Shows how well management is serving the equity holders. | Business Efficiency: Shows the true strength of the business engine and operational efficiency, regardless of how it is funded. |

| Investor Trap | The Leverage Trap: A high ROE might hide a mountain of risky debt. | The Efficiency Trap: A declining ROCE over time signals the company is losing its competitive advantage (moat). |

How to Use ROE and ROCE in Investment Decision-Making

Treating ROE and ROCE as a two-step filter is a useful approach to apply them. Check what gets to shareholders after checking the engine.

- To assess business strength, begin with ROCE: Inquire as to whether the business is making a profit on the capital it requires to operate. A steady ROCE is frequently an indication of pricing power, operational discipline, or competitive strength.

- Determine the shareholder outcome using ROE: Once interest, taxes, and capital structure decisions have been made, how much of that company's performance is translated into shareholder returns? You may see the outcome for equity stockholders with the aid of ROE.

- Keep an eye out for typical ROE & ROCE traps: When equity falls abnormally low due to aggressive accounting, write-offs, or buybacks, ROE may be misleading. Debt increases significantly, and one-offs (transient gains that cover for poorer operations) increase profits, which makes ROE and ROCE both misleading.

- Examine trends rather than just results over a single year: A multi-year perspective is usually preferred by analysts, by asking a few questions like Is ROCE increasing, staying the same, or declining? Does ROE fluctuate more than its peers or the industry average? This multi-period approach aids in assessing the actual performance of a business since prudent investment typically favours consistency over reaction.

Conclusion

Returning to our house analogy, ROE tells you that your rental income is great compared to your small down payment. But ROCE reminds you that you owe the bank a fortune, and if the rent drops, you might lose the house.

In the world of Quality Investing, ROE is a great headline, but ROCE is the fine print that tells the real story. To build a portfolio that stands the test of time, you need to look beyond simple profitability. By balancing ROE with ROCE, you ensure that you aren't just buying growth, but buying sustainable, resilient, and efficient businesses. True wealth isn't just about how fast you go; it's about how safely you can keep moving forward.

FAQs

Q) Is it possible for a business to have a high ROE and a poor ROCE?

Indeed. This usually occurs when a business has a large debt load. Although the overall efficiency of the capital (ROCE) may be low, the debt increases returns for shareholders (ROE) by decreasing the equity base. For quality investing, this is frequently a warning sign.

Q) What connection does the Quality Factor have with these ratios?

Both are essential components of the Quality Factor. In order to ensure that profitability is generated by business efficiency rather than excessive financial leverage, quality strategies usually search for companies with high and consistent ROE and ROCE.

Q) Should I disregard ROE entirely?

No, ROE is a crucial indicator of shareholder return. Combining ROE and ROCE is the most effective strategy. The gold standard of a high-quality company is a strong ROE backed by a robust ROCE.

Investors are requested to take advice from their financial/ tax advisor before making an investment decision.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.