Behavioural Biases in Investing: How They Impact Your Decisions

Investing is not just about logic and data; it’s also shaped by human psychology. In our previous blog on biases in behavioural finance, we explored how Hot Hand Fallacy, Naive Diversification, and Recency Bias influence investor decisions. These behavioural biases in investing often lead to irrational financial choices, such as chasing past performance, diversifying without strategy, or overemphasising recent trends.

In this second part of our series on behavioural biases in investment decision-making, we continue uncovering psychological biases that impact investor choices.

Common Biases in Investing

1. Status Quo Bias

Status quo bias in investing refers to the tendency of investors to prefer things to stay the same or stick with what they are already doing, rather than making changes or adapting to new opportunities. This often results in a reluctance to adjust portfolios despite evolving market conditions. Further highlighting the importance of strategies such as smart beta investing and factor-based investing, which focus on systematic adjustments based on market conditions.

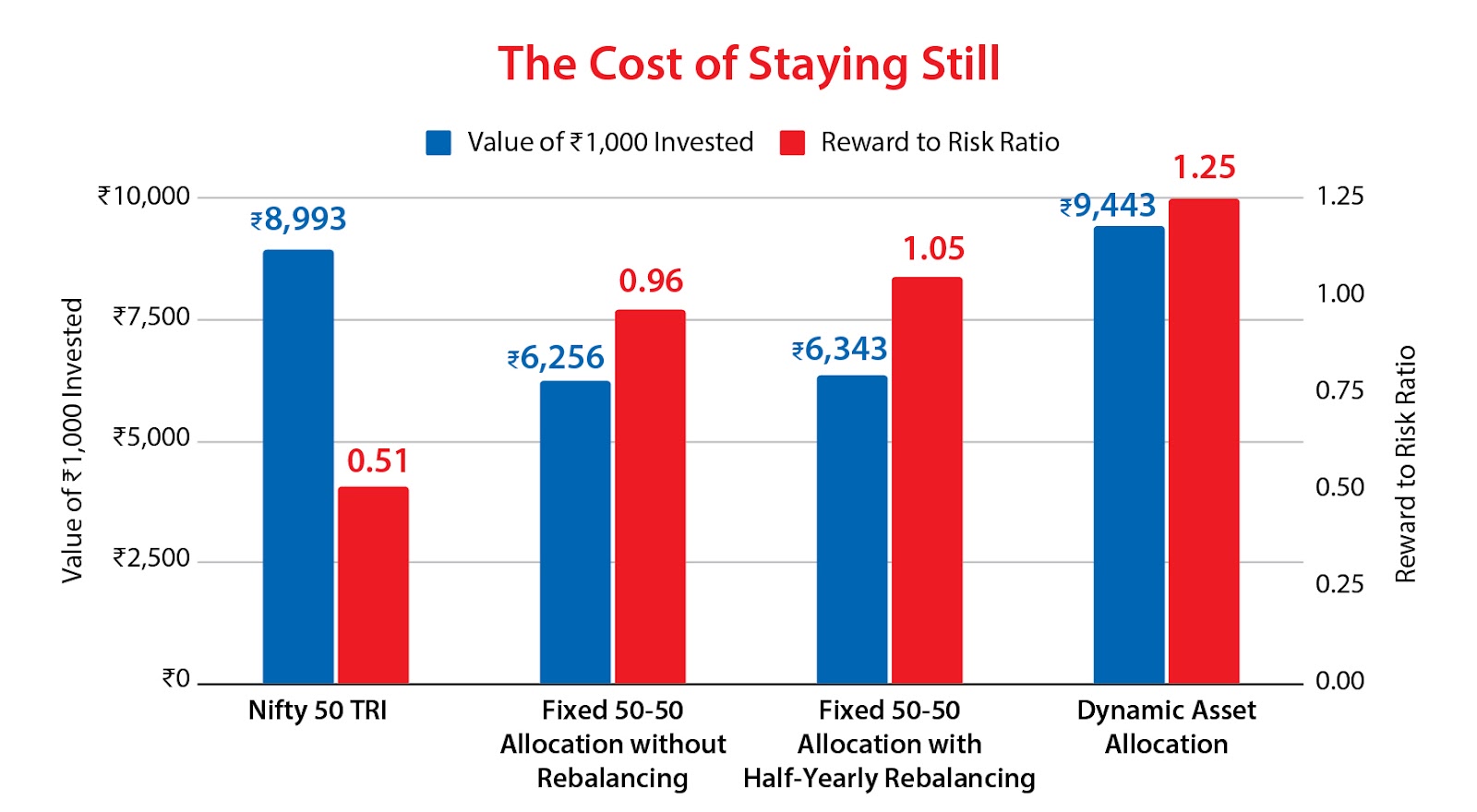

The following graph comparing different asset allocation strategies reveals that a dynamically adjusted portfolio based on pre-determined rules delivers higher returns and a better reward-to-risk ratio than a fixed 50-50 allocation and Nifty 50. Investors who fail to adapt due to status quo bias may find themselves with underperforming portfolios that do not align with market realities.

Source: NSE, CMIE. For the period of 30th September 2006 to 30th September 2024. The "Fixed 50-50 Allocation without Rebalancing", "Fixed 50-50 Allocation with Half-Yearly Rebalancing" and "Dynamic Asset Allocation" are the proprietory asset allocation models of NJ Asset Management Private Limited. In "Fixed 50-50 Allocation without Rebalancing", 50% is allocated into Equity and Debt each at the start of the period. In "Fixed 50-50 Allocation with Half-Yearly Rebalancing", 50% is allocated into Equity and Debt each at the start of the period and the asset allocation is rebalanced on an half-yearly basis. In "Dynamic Asset Allocation", allocations into Equity and Debt each at the start of the period and on half-yearly basis is determined based on market valuations. Equity returns are represented by returns of Nifty 50 TRI whereas Debt returns are represented by the unannualised 1 month average yield of the 3Yr Indian G-Sec. Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Takeaway: Don’t let inertia dictate your investment decisions. Regularly review your portfolio and make adjustments based on market conditions and financial goals.

2. Herd Mentality Bias

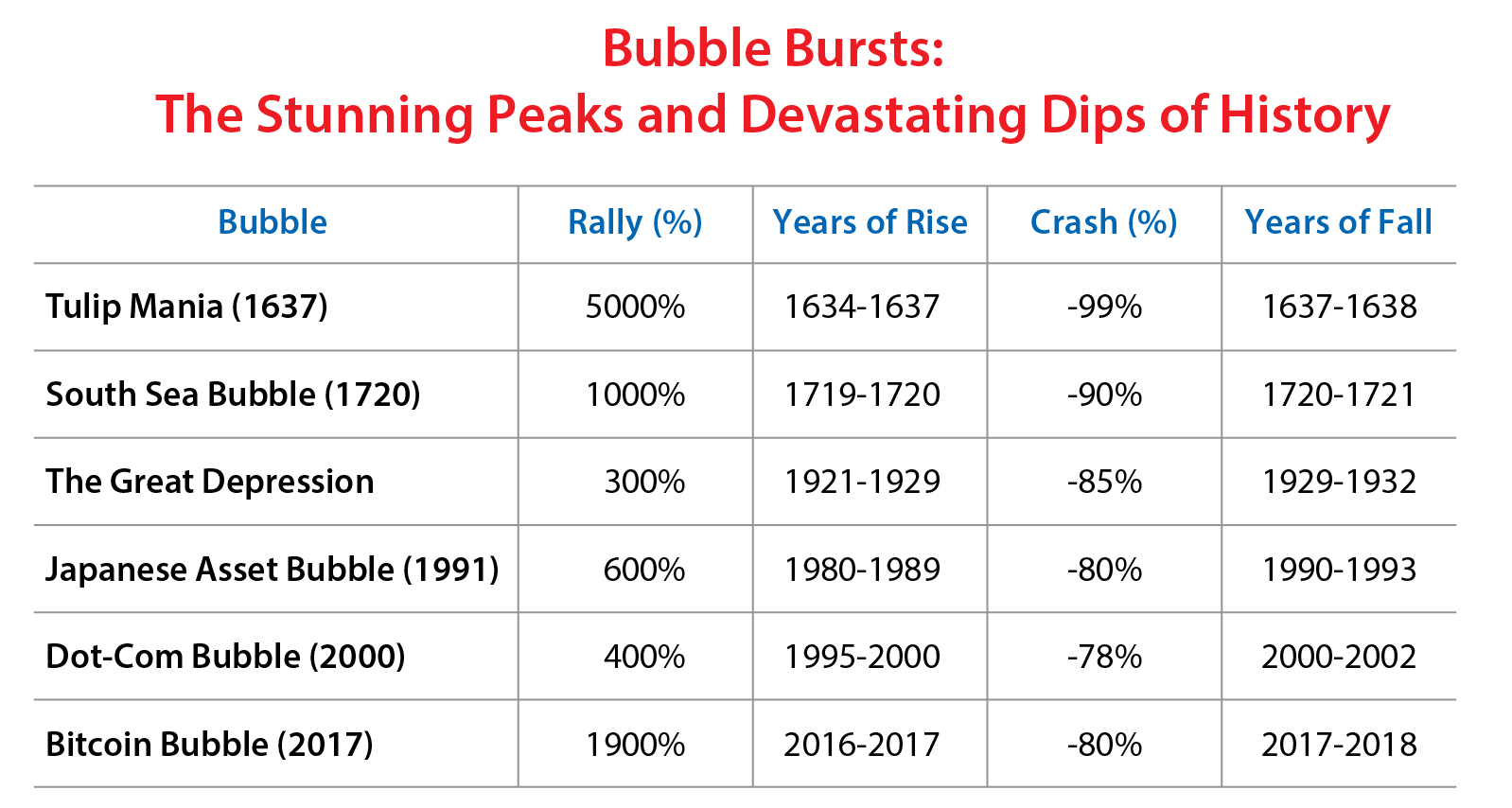

Herd mentality bias in investing refers to the tendency of individuals to follow the actions or decisions of the majority, often ignoring their analysis or judgment. This tendency often leads to speculative bubbles, market crashes, and irrational financial decisions.

From the Tulip Mania to the Dot-com Bubble and the rise and fall of cryptocurrencies, one thing remains clear, herd mentality bias drives irrational investment behaviour. Fear of missing out (FOMO) pushes investors into speculative purchases, often leading to overvalued assets. When the bubble inevitably bursts, losses are significant for those left holding overpriced investments.

Source: Tulip Mania: Research by historian Mike Dash in "Tulipomania: The Story of the World's Most Coveted Flower." South Sea Bubble: Data from Charles Kindleberger's "Manias, Panics, and Crashes." Stock market and dot-com data: Robert J. Shiller's "Irrational Exuberance." Bitcoin: Historical price trends from cryptocurrency databases (CoinMarketCap). The Great Depression: “The Great Crash 1929” by John Kenneth Galbraith. Japanese Asset Bubble: “Princes of the Yen” by Richard Werner. Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Takeaway: Avoid investment decisions based on hype. Instead, opt for a quality-focused strategy that emphasises strong fundamentals and long-term growth rather than short-term trends.

3. Overconfidence Bias

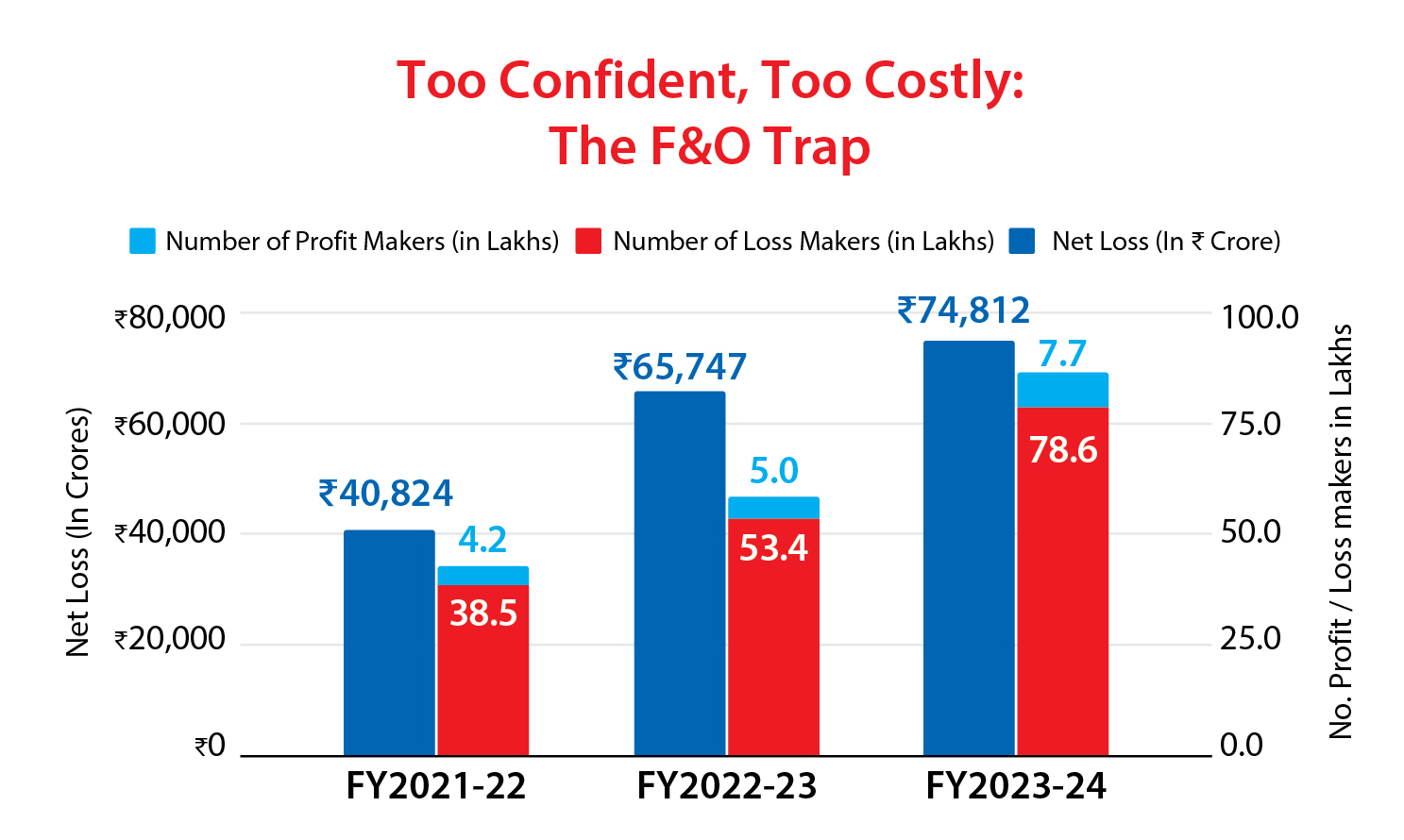

Overconfidence bias leads investors to overestimate their ability to predict market movements, often resulting in excessive risk-taking and overtrading.

A SEBI report on futures and options (F&O) trading found that 91.1% of individual traders incurred losses in FY 2023-24, despite the number of participants doubling over two years. Many traders, especially younger investors from B30 cities, continued trading despite repeated losses, believing they could outsmart the market. This illustrates the dangers of overconfidence bias, further reinforcing the need for investing strategies like low volatility factor investing, which aims to minimise downside risk while generating stable returns.

Source: SEBI 2024 report "Analysis of Profits & Losses in the Equity Derivatives Segment (FY22-FY24)". Number of Loss Makers is calculated by multiplying the number of total traders with proportion of loss makers for the respective period. Number of Profit Makers is calculated by subtracting the Number of Loss Makers from the number of total traders. Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Takeaway: Confidence is important, but unchecked overconfidence can be costly. Stick to disciplined, long-term investment strategies and avoid excessive speculation.

Conclusion

Behavioural biases in investing can significantly impact investment outcomes. Status quo bias may lead to inertia, herd mentality bias can result in irrational market participation, and overconfidence bias can encourage excessive risk-taking.

The NJ Mutual Fund Investment Calendar 2025 is a practical tool for helping investors recognize and counteract behavioural finance biases. It offers insights into behavioural finance biases and strategies for building a more resilient investment plan. Using this calendar as a guide, investors can develop disciplined habits and make more objective financial decisions.

FAQs

Q) How does status quo bias impact investment decisions?

Status quo bias causes investors to resist portfolio adjustments, even when market conditions change. This reluctance can lead to underperformance as investments fail to align with evolving financial goals and economic trends.

Q) What are the risks of herd mentality bias in investing?

Herd mentality bias leads investors to follow market trends without independent analysis, often resulting in speculative bubbles and significant losses when overvalued assets crash.

Q) Why is overconfidence bias dangerous for investors?

Overconfidence bias makes investors overestimate their ability to predict markets, leading to excessive trading and risk-taking.

Investors are requested to take advice from their financial/ tax advisor before making an investment decision.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

« Previous Next »