Understanding Common Behavioral Biases That Hurt Your Portfolio

Investing is as much a psychological game as it is a financial one. Investors often assume they make rational decisions based on logic and data. However, in reality, human psychology plays a major role in shaping investment choices. Behavioural biases in investing can lead to suboptimal decisions, impacting portfolio returns over time.

In our previous blogs, we explored various behavioural biases that affect investment decisions, highlighting how psychological tendencies influence financial choices. Continuing this discussion, let’s explore the other four key behavioural biases.

Common Biases in Investing

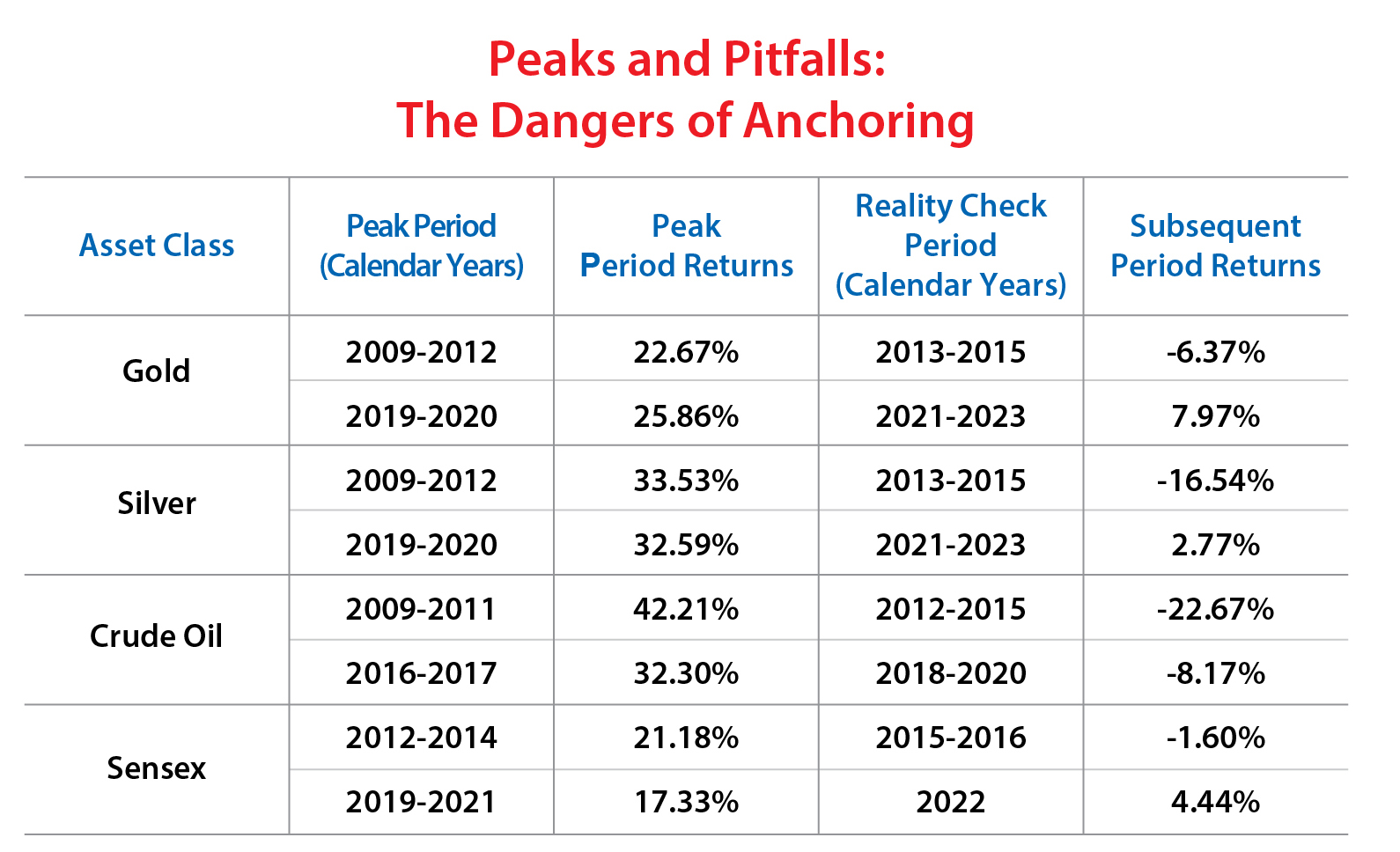

1) Anchoring Bias

One of the most common behavioural biases in investment decision-making is anchoring bias, where investors rely too heavily on the first piece of information they receive when making decisions.

For example, the impressive growth in gold and Sensex over the past few years led many investors to believe that such high returns would continue for subsequent periods. However, historical data suggests that periods of strong performance are often followed by phases of correction or stagnation. Those who based their future expectations on past peaks were later disappointed, which is why investment strategies like factor investing help maintain a disciplined approach.

Source: CMIE, Bloomberg Intelligence. Performance of all the asset classes is represented by their Annualized Returns. Performance of Gold, Silver and Crude Oil are represented by MCX India Gold Spot Index (MCI), MCX India Silver Spot Index (MCI), Crude Oil Dated Brent FOB NWE respectively. Sensex Total Return Index is used for Sensex Performance. Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Takeaway: Avoid basing investment decisions solely on recent performance. Instead, take a long-term approach and evaluate fundamental factors rather than short-term surges.

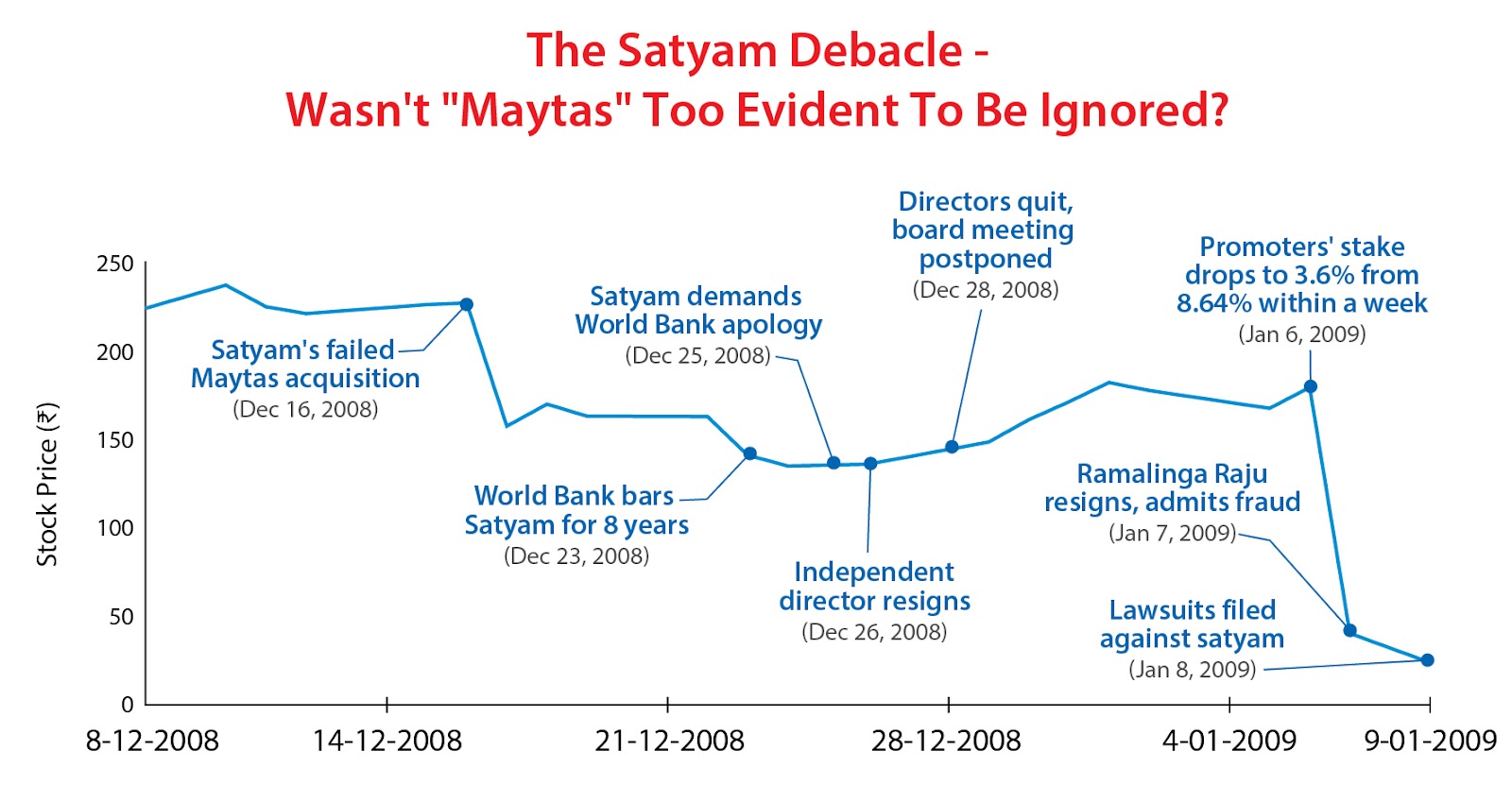

2) Confirmation Bias

Confirmation bias is the tendency to seek out information that confirms pre-existing beliefs while ignoring contradictory evidence. This psychological bias in financial investment behaviour can cause investors to overlook risks.

The Satyam scandal serves as a classic case of confirmation bias. Investors ignored multiple warning signs, such as high promoter pledges, excessive auditor fees, and unrealistic cash reserves, because they were captivated by the company’s growth narrative​. Even when Satyam’s failed acquisition of Maytas Infra raised suspicions, investors remained optimistic. When the fraud was exposed in 2009, the stock crashed by over 90%, leaving investors with massive losses.

Source: CMIE, The Economic Times (New Delhi, 08-01-2009). The stock price shown in chart is from 8th December 2008 to 9th January 2009. Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Takeaway: Incorporating forensic and governance analysis can help identify potential risks early, ensuring that investment decisions are based on strong fundamentals rather than narratives.

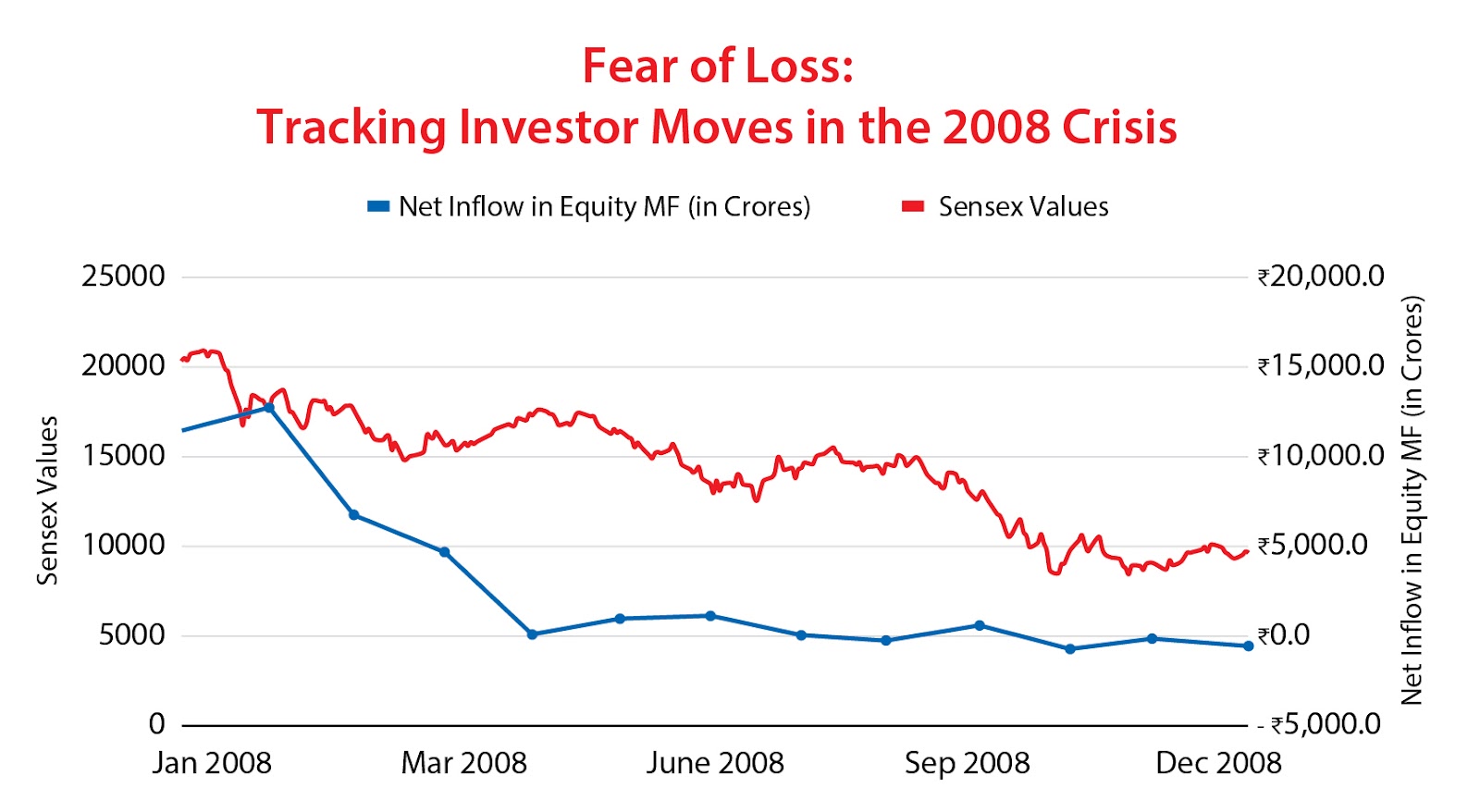

3) Loss Aversion Bias

Loss aversion bias suggests that investors tend to feel the pain of losses more intensely than the joy of gains, leading them to hold on to underperforming assets in the hope of recovery.

For example, during the 2008 market crisis, data shows how loss aversion bias drove investor behaviour. In October 2008, while the Sensex dropped to 9,788.06 (> 50% fall), equity mutual fund net inflows plummeted sharply (> 100% fall), indicating that fear of further losses led investors to sell off.

Source: BSE, AMFI Monthly Report. Data from January 2008 to December 2008. Till June 2008, the total net inflow / outflow in "Growth" category is considered. From July 2008 onwards, total net inflow / outflow in "Equity" category is considered. The Sensex Price Return Index is used for Sensex Values. Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Takeaway: Don’t let the fear of losses dictate your decisions. Evaluate investments based on their future potential and not past performance.

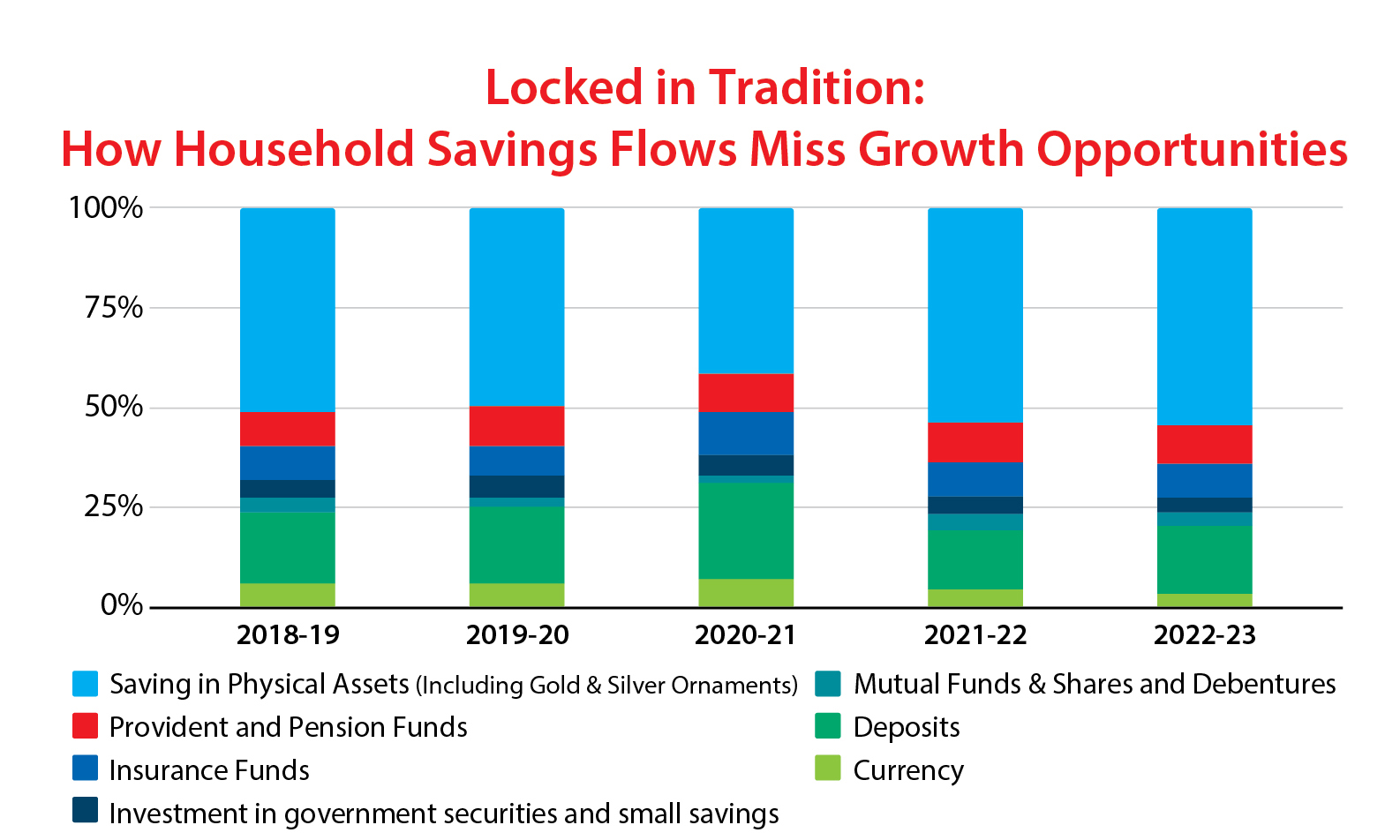

4) Conservatism Bias

Conservatism bias is a cognitive bias where individuals tend to cling to their prior beliefs or forecasts and underreact to new information. Instead of adjusting their views promptly when new evidence emerges, they update their beliefs too slowly, leading to suboptimal decision-making.

A key example of Conservatism Bias can be observed in the way Indian households allocate their savings. As seen in the below graph, Indian households have historically preferred traditional saving instruments like fixed deposits, gold, and real estate, despite the consistent long-term outperformance of equity markets.

Source: BSE, RBI, Office of The Economic Advisor, Ministry of Statistics and Programme Implementation (MOSPI). The proportion of household flows in various asset classes shown in chart is for FY 2018-19 to FY 2022-23. Value of Rs. 1,000 Invested as on 31st March 2024. Sensex PRI is used as a proxy for equities. Gold represents the average annual price of gold in India per 10gm from FY 1981-82 to FY 2023-24. Average of 1 to 3 Year Fixed Deposit (FD) Rates published by RBI have been used to calculate the FD returns. The FD rates relate to that of the 5 major public sector banks up to 2003-04, post which they represent the deposit rate of the 5 major banks. Past performance may or may not be sustained in future and should not be used as a basis for comparison with other investments.

Takeaway: Be adaptable and open to new financial insights. Rely on data-driven decision-making rather than outdated beliefs to navigate evolving market trends effectively.

Overcoming These Behavioral Biases in Investing

Investors can stay on the right path by focusing on fundamental strength, long-term wealth creation, and objective decision-making.

- Following a structured investment process: Making investment decisions based on data rather than emotions.

- Emphasising quality investing: Prioritizing fundamentally strong businesses rather than reacting to short-term market fluctuations.

- Staying committed to long-term goals: Avoid impulsive decisions driven by short-term market noise.

- Diversifying investments: Ensuring a well-balanced portfolio to mitigate risk, similar to multi-factor investing.

Conclusion

Behavioural biases in investment decision-making can significantly impact financial outcomes. By understanding and addressing these biases, investors can make more rational and informed decisions. Whether it's avoiding anchoring to past prices, seeking diverse viewpoints, managing loss aversion, or adapting to new information, overcoming these psychological hurdles can lead to better financial success.

With key insights into different psychological biases that affect investing decisions, the NJ Mutual Fund Investment Calendar 2025 helps investors stay informed and make objective, well-reasoned choices throughout the year.

FAQs

Q) What are the different types of biases in behavioural finance that affect investing?

Behavioural finance biases, such as anchoring bias, confirmation bias, loss aversion bias, and conservatism bias, influence investment decision-making by causing irrational choices based on emotions and past experiences.

Q) How does loss aversion bias impact investment decisions?

Loss aversion bias leads investors to fear losses more than they value gains, often resulting in holding onto losing investments too long or avoiding necessary risk-taking for portfolio growth.

Q) How can investors overcome behavioural biases in finance?

Investors can overcome behavioural biases by adopting a rule-based investment approach, focusing on quality investing, diversifying their portfolios, and maintaining a long-term perspective to avoid emotional decision-making.

Investors are requested to take advice from their financial/ tax advisor before making an investment decision.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

« Previous Next »