Breaking Myths About Quality Investing

Introduction

Imagine walking through a supermarket where products with shiny packaging instantly catch your eye. They look appealing, promising, and better because of how they look. But when you check the ingredients, you often discover that the simple-looking product is actually healthier and more nutritious than that catchy product due to the packaging.

Quality investing works just like this. At first glance, companies that deliver consistent earnings, maintain healthy balance sheets, and follow disciplined governance may not always seem exciting at first sight. But these companies show much better resilience and consistency and generate long-term wealth.

Unfortunately, there are a number of myths that have arisen around quality investing. Because of this, investors often fail to see its true value, resulting in actions being taken on hype instead of facts. These myths often prevent investors from understanding quality investing and its benefits.

Myth 1: Quality investments are worth buying at any price.

Investors generally believe that when you are investing in a high-quality portfolio, it can be bought at any price and still do well. On the surface, it sounds comforting: strong business, strong brand, strong future. But in investing, what you pay matters just as much as what you buy.

A company can have strong financials, consistent profit growth, low debt, and sound governance, yet still be too expensive. Quality works best when it is paired with a reasonable price (QARP). The idea is not just to chase high-quality companies but also to buy them at the right price. Therefore, quality is important. But quality at any price? That’s a myth worth leaving behind.

For the period of 30th September 2006 to 31st July 2025, the QARP Model delivered a return of 18.38% with 16.66% volatility, versus 15.68% and 18.84%, respectively, for the NJ Enhanced Value Model and 12.69% and 20.06%, respectively, for the Nifty 500 TRI, while having a lower drawdown.

Myth 2: Quality Investing Delivers Lower Returns

Many investors assume that quality investing generally prioritizes safety while neglecting returns. However, long-term data across global and Indian markets show that quality delivers better risk-adjusted returns by limiting downside with steady compounding.

Quality portfolios may not deliver sudden spikes, but avoid sharp declines, one of the most effective ways to build long-term wealth.

| From Sep 2006 to Oct 2025 | Cumulative Growth of ₹1000 | Annualised Volatility (%) | 5-Year Period Loss Probability (%) |

| NJ Quality+ | ₹28,806 | 16.78 | 0.00 |

| Low Quality Model | ₹5,523 | 22.76 | 16.86 |

| Nifty 500 TRI | ₹9,857 | 19.96 | 1.15 |

Source: Internal research, CMIE, NSE. The period for calculation is 30th September 2006 to 31st October 2025. Past performance may or may not be sustained in future and is not an indication of future return. NJ Quality+ Model and Low Quality Model are proprietary methodologies developed by NJ Asset Management Private Limited. The methodology will keep evolving with new insight based on the ongoing research and will be updated accordingly from time to time.

Myth 3: Quality Investing Doesn’t Perform in Bull Markets

A common belief is that quality portfolios lag in strong bull markets because they avoid speculative names. But the reality is that quality investing works reasonably well across market cycles. While quality doesn’t avoid market participation, it simply avoids speculative stocks. Reality is that the quality participates in the market without taking unnecessary risk.

During bull phases, high-quality businesses benefit from the growth environments, strong balance sheets. During the bull phase, they may not be the fastest movers, but they often offer more durable performance and avoid reversals during market corrections.

Myth 4: Quality Investing Means Focusing Only on Large, Safe, Old Companies

Quality investing does not mean investing in only large or mature businesses. Many mid-cap and small-cap companies also show the characteristics of being a high-quality company.

Quality is not identified through market cap but through metrics. A business might be small in size but still be high in quality, and history shows that multiple long-term wealth creators started as small and quality-focused companies before evolving into market leaders.

Myth 5: High growth means high quality.

High growth is often mistaken for a sign of high quality, but the two are not the same. A company may grow rapidly for a few years due to favourable business cycles, aggressive expansion, or short-term trends, but still lack the financial strength or stability that defines true quality. True quality is not just in how fast a company grows but in how reliably and responsibly it grows over time.

Quality is rooted in consistent profitability, strong balance sheets, disciplined capital allocation, and durable business models. Growth, on the other hand, can be temporary, volatile, or driven by external factors that may not last. Depending solely on growth can mislead investors into chasing companies that look impressive today but struggle to sustain performance when conditions change.

For the period of 30th September 2006 to 31st July 2025, quality has outperformed growth, with the high-quality model delivering the highest return (19.53%), lowest volatility (16.84%), shallowest drawdown (–59.05%), and a 0% 5-year loss probability. In contrast, Growth portfolios, be it revenue growth or EPS growth, show higher volatility, deeper drawdowns, and higher loss probabilities, despite moderate returns.

Myth 6: Quality Investing Is Just Another Temporary Trend

Quality investing has decades of global academic and empirical evidence proving its performance. In multiple regions across the globe, quality has consistently shown resilience and stability. Quality investing succeeds by focusing on the strong fundamentals, not fads.

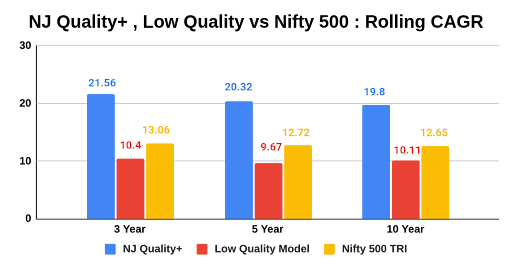

Source: Internal research, CMIE, NSE. Average of daily rolling returns calculated for the different holding periods. The period for calculation is 30th September 2006 to 31st October 2025. Past performance may or may not be sustained in future and is not an indication of future return. NJ Quality+ Model and Low Quality Model are proprietary methodologies developed by NJ Asset Management Private Limited. The methodology will keep evolving with new insight based on the ongoing research and will be updated accordingly from time to time.

As shown in the chart above, the NJ Quality+ model has outperformed both the Low Quality model and the Nifty 500 TRI across 3-year, 5-year, and 10-year rolling periods. For instance, over a 10-year rolling horizon, evidence of quality is not just a passing trend.

Conclusion

Just like judging food by packaging leads to poor choices, judging businesses based on myths leads to missed opportunities. Quality investing is built on fundamentals, not assumptions.

When investors look beyond hype and myths, they discover companies capable of delivering long-term stability, resilience, and compounding, along with building lasting wealth. Knowing what’s real beyond these myths builds a base for focused, stable, and relevant investment because ultimately, long-term success is determined by the inherent strength of the business, not the surrounding narrative.

FAQs

Q) Does quality only work in volatile markets?

No. It works across market cycles by providing protection during downturns and supporting steady participation during rallies.

Q) Can quality be applied across different market caps?

Absolutely. Quality businesses exist across large, mid, and small-cap segments.

Q) How long should one stay invested for quality to work?

Quality investing works best over multi-year horizons where compounding can fully express itself.

Investors are requested to take advice from their financial/ tax advisor before making an investment decision.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

« Previous Next »